Navigating debt can feel overwhelming, especially with rising costs and economic uncertainty. Many are seeking effective ways to manage their financial burdens. This article explores debt consolidation and relief options available in 2026, providing clarity and practical advice for those looking to regain control of their finances.

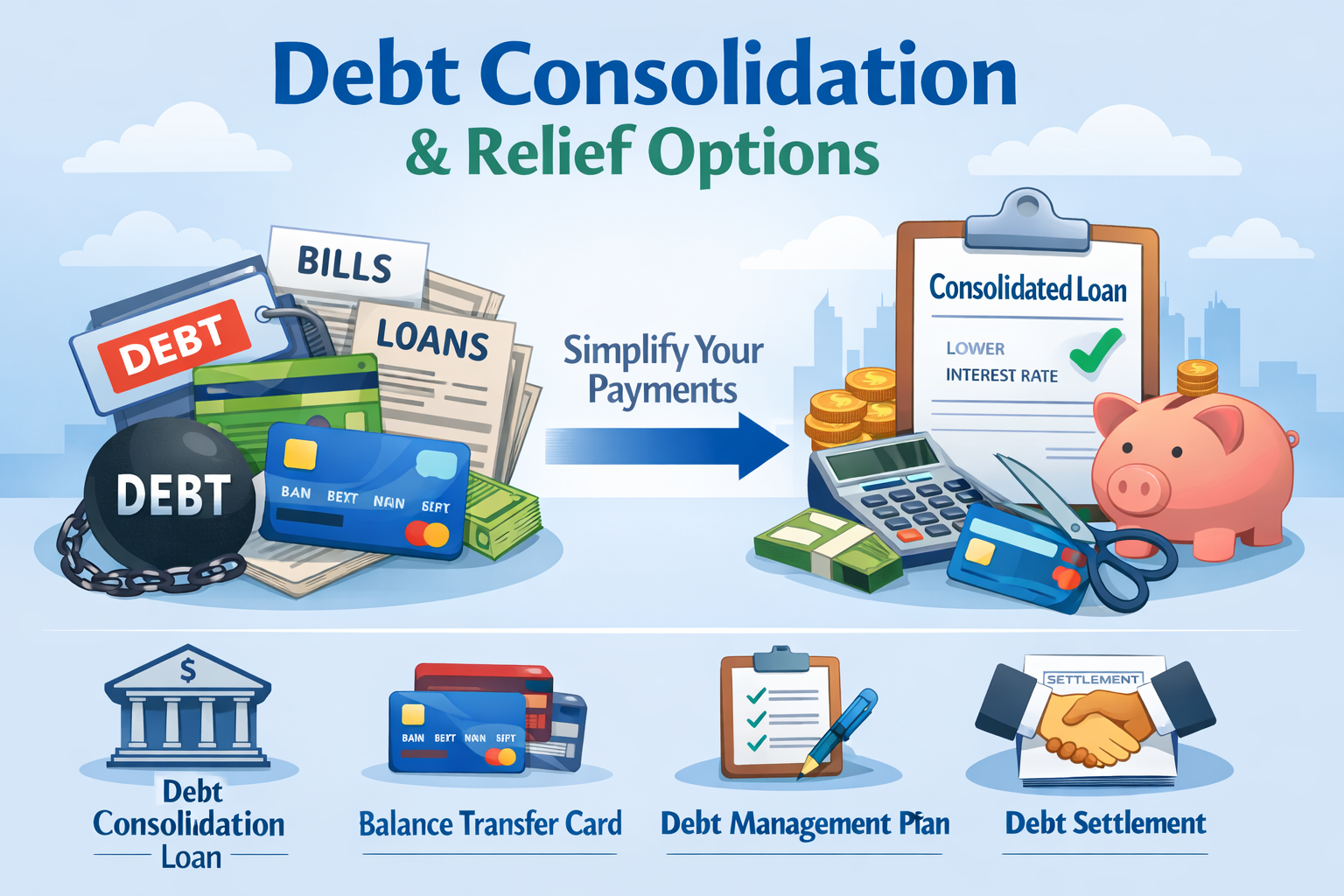

What is Debt Consolidation?

Debt consolidation is a financial strategy that involves combining multiple debts into a single loan or payment. This can simplify monthly payments and potentially lower interest rates. By consolidating, individuals can focus on one payment instead of juggling several, which can reduce stress and improve financial management.

Common methods of debt consolidation include personal loans, balance transfer credit cards, and home equity loans. Each option has its pros and cons, so it's essential to evaluate which method aligns best with personal financial situations.

Benefits of Debt Consolidation

One of the primary benefits of debt consolidation is the potential for lower interest rates. By securing a loan with a lower rate than existing debts, individuals can save money over time. Additionally, having a single monthly payment can make budgeting easier and help avoid missed payments, which can lead to further debt.

Moreover, debt consolidation can improve credit scores over time. By reducing the number of open accounts and making consistent payments, individuals may see a positive impact on their credit history.

Debt Relief Options to Consider

In addition to debt consolidation, there are various debt relief options available. Debt settlement involves negotiating with creditors to reduce the total amount owed. While this can provide immediate financial relief, it may also negatively impact credit scores and should be approached with caution.

Another option is credit counseling, where professionals help create a personalized plan to manage debt. This can include budgeting advice and negotiating with creditors on behalf of the individual. It's a supportive approach that can empower individuals to take control of their financial situation.

Understanding the Risks

While debt consolidation and relief options can be beneficial, they are not without risks. For instance, consolidating debt can lead to a longer repayment period, which may result in paying more interest over time. It's crucial to read the fine print and understand the terms of any new loan or agreement.

Additionally, some debt relief options, like settlement, can lead to tax implications. The forgiven debt may be considered taxable income, which can create further financial challenges. Consulting with a financial advisor can help clarify these risks and guide informed decisions.

Steps to Take Before Choosing an Option

Before deciding on a debt consolidation or relief option, it's essential to assess personal financial situations. This includes reviewing income, expenses, and total debt. Creating a budget can provide insight into what is manageable and help identify the best course of action.

Researching different lenders and relief programs is also vital. Comparing interest rates, fees, and terms can lead to better choices. Seeking advice from financial professionals can provide additional support and ensure that decisions are well-informed.